Pension Pot Emptying Rise: Why Retirees Are Running Out of Savings Faster

In 2024-25, 462,160 pension pots were fully withdrawn when first accessed, a 29pc rise from 357,122 in 2018-19, according to Financial Conduct Authority (FCA) data.

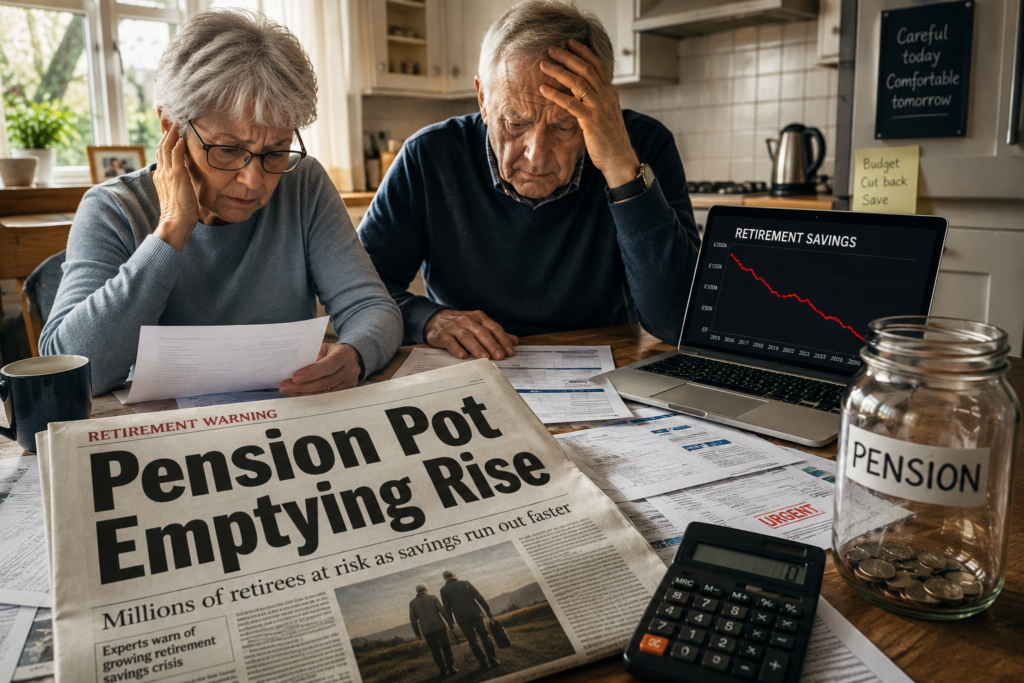

Retirement is supposed to be the stage of life where years of hard work finally provide financial comfort and stability. But for a growing number of retirees, that security is starting to disappear much sooner than expected. Across the UK and other countries with flexible retirement systems, pension pots are being emptied at a faster pace, raising concerns among financial experts and policymakers alike.

The trend has become known as the “pension pot emptying rise” — a situation where retirees withdraw large amounts from their retirement savings early on, sometimes leaving themselves financially vulnerable later in life.

With inflation, rising living costs, longer life expectancy, and flexible pension access all playing a role, many people are now questioning whether modern retirement savings are built to last.

What Does “Pension Pot Emptying Rise” Mean?

A pension pot is the savings fund people build during their working years to support themselves after retirement. Traditionally, pensions were designed to provide a stable income over decades. However, modern pension rules in the UK allow retirees to access their money much more freely after the age of 55.

While this flexibility offers freedom and control, it has also created a new financial risk. Many retirees are withdrawing too much money too quickly, causing their pension savings to shrink faster than expected.

Some people use their pension to:

- Pay off debts

- Cover rising household expenses

- Help family members financially

- Fund travel and lifestyle upgrades

- Handle emergency costs

The problem is that retirement often lasts much longer than people initially expect.

Why Are Pension Pots Emptying Faster?

Rising Cost of Living

One of the biggest reasons behind the increase is the cost-of-living crisis. Everyday essentials such as food, electricity, healthcare, and housing have become significantly more expensive in recent years.

Many retirees living on fixed incomes are forced to dip deeper into their pension savings simply to maintain their standard of living.

Inflation can quietly reduce purchasing power over time, making retirement far more expensive than people planned for years earlier.

Pension Freedom Rules

The UK’s pension freedom reforms introduced in 2015 gave people more flexibility over how they use their retirement savings. Instead of buying guaranteed lifetime annuities, retirees could withdraw large sums whenever they wanted.

Although the policy increased financial freedom, it also removed some safeguards that once prevented overspending.

For some retirees, easy access to large amounts of money has encouraged withdrawals that may not be sustainable over the long term.

Longer Life Expectancy

People are now living longer than previous generations. A person retiring in their mid-60s may need their pension savings to last 25 to 30 years or even longer.

Unfortunately, many retirement plans were not built around such long timeframes.

If withdrawals are too high during the early years of retirement, savings can disappear much sooner than expected.

Lack of Financial Planning

Retirement income planning can be complicated, and many people approach it without professional advice.

Some retirees underestimate:

- Future living expenses

- Healthcare costs

- Inflation impact

- Investment risks

- Longevity

Without a proper withdrawal strategy, pension savings can quickly become difficult to manage.

Lifestyle Spending

For some people, retirement feels like a reward after decades of work. That often leads to larger spending during the first few retirement years.

Common examples include:

- Luxury holidays

- Home renovations

- Buying new vehicles

- Financial gifts to children or grandchildren

While these expenses may seem manageable at first, they can place long-term pressure on retirement savings.

The Biggest Risks of Emptying a Pension Pot Early

Running Out of Retirement Income

The most serious danger is simply exhausting retirement savings too early.

If pension funds disappear in a person’s 70s, they may still face another 10 to 20 years of living expenses with limited income sources available.

Increased Dependence on State Support

Once private pensions are depleted, many retirees become more dependent on:

- State pensions

- Government support programs

- Family assistance

This can create financial pressure not only for retirees but also for younger family members.

Reduced Investment Growth

When large amounts are withdrawn early, less money remains invested for future growth.

Over time, retirees may lose the benefits of compound returns that could have helped their pension continue growing during retirement.

Higher Tax Bills

Large pension withdrawals can also trigger unexpected tax consequences.

Taking too much money in a single tax year may push retirees into a higher income tax bracket, reducing the actual amount they keep.

Pension Drawdown vs Annuity

Pension Drawdown

Drawdown allows retirees to keep their pension invested while withdrawing money gradually.

Benefits include:

- Flexible income

- Investment growth potential

- Greater control over savings

However, poor withdrawal management can increase the risk of running out of money.

Annuities

An annuity provides guaranteed income for life in exchange for pension savings.

Benefits include:

- Stable monthly income

- Reduced financial uncertainty

- Protection against outliving savings

The downside is reduced flexibility and lower returns during periods of high inflation.

Why Experts Are Concerned

Financial experts are increasingly warning about a future retirement savings crisis.

Several concerns continue to grow:

- More retirees living longer with limited savings

- Inflation reducing purchasing power

- Healthcare and care-home costs rising

- Younger generations struggling to save enough for retirement

Experts also worry that many people underestimate how expensive retirement truly is in modern economies.

Signs Your Pension Pot Could Run Out Too Early

Some warning signs include:

- Frequent large withdrawals

- No retirement budget

- Heavy reliance on pension money for daily expenses

- Minimal emergency savings

- Poor investment diversification

- Continuing debt during retirement

Recognizing these signs early can help retirees adjust their financial plans before problems become severe.

How Retirees Can Make Their Pension Last Longer

Create a Retirement Budget

A clear budget helps retirees track spending and avoid unnecessary withdrawals.

Withdraw Money Gradually

Taking smaller amounts over time can help pension savings last longer.

Keep Some Investments Active

Maintaining part of the pension in investments may support long-term growth.

Delay Major Purchases

Avoiding expensive lifestyle spending during the early retirement years can preserve savings.

Seek Professional Financial Advice

Professional retirement planning can help retirees balance income needs with long-term financial security.

Review Retirement Plans Regularly

Retirement needs change over time. Regular financial reviews can help identify risks early.

The Future of Retirement Savings

The rise in pension pot emptying highlights a larger issue facing modern retirees. As living costs increase and life expectancy continues to grow, retirement planning is becoming more challenging than ever.

Financial experts believe future retirees may need:

- Larger pension savings

- Longer working careers

- Smarter investment strategies

- More disciplined withdrawal plans

Without better planning, more retirees could face financial difficulties later in life.

Interesting Facts About Pension Pot Emptying

- Many retirees access pension savings before the age of 65.

- Flexible pension access became more common after the 2015 pension reforms.

- Inflation is one of the biggest threats to retirement purchasing power.

- Healthcare costs often rise sharply during later retirement years.

- Financial experts frequently recommend diversified retirement income sources.

FAQs

What does pension pot emptying mean?

It refers to retirees withdrawing retirement savings too quickly, causing pension funds to run out earlier than planned.

Why are retirees withdrawing pensions faster?

The main reasons include rising living costs, pension freedom rules, inflation, and lifestyle spending.

Can you run out of pension money?

Yes. Without careful planning, retirees can fully exhaust their pension savings during retirement.

Is pension drawdown risky?

Drawdown offers flexibility, but poor withdrawal management can increase the risk of running out of money.

What happens if a pension pot becomes empty?

Retirees may need to rely on state pensions, family support, or other income sources.

Are annuities safer than drawdown?

Annuities provide guaranteed income for life, while drawdown offers more flexibility but higher risk.

Insights

The growing rise in pension pot emptying is becoming a serious concern for retirees and financial experts alike. Flexible pension access has given people more freedom over their savings, but it has also increased the risk of spending retirement funds too quickly.

As living costs continue to rise and people live longer than previous generations, careful retirement planning has never been more important. Retirees who manage withdrawals wisely, maintain long-term investment strategies, and seek professional advice are more likely to protect their financial security throughout retirement.